Revolut Report: Stats indicate a return to Irish staycations this summer

Revolut, the European-licensed bank with more than 45 million customers worldwide, and over 2.8 million in Ireland, has crunched the…

Leading real hands on tech review site in Ireland with technology, business news and more. Jim O Brien Tech.

Revolut, the European-licensed bank with more than 45 million customers worldwide, and over 2.8 million in Ireland, has crunched the…

Fenergo, the leading provider of digital solutions for Know Your Customer (KYC), Transaction Monitoring (TM) and Client Lifecycle Management (CLM),…

Bank of Ireland Finance has been announced as the exclusive finance partner of the all-electric motor franchise Smart – with…

Small and medium-sized enterprises (SMEs) in Ireland that sell online appear to be experiencing a growth period, with 96 per…

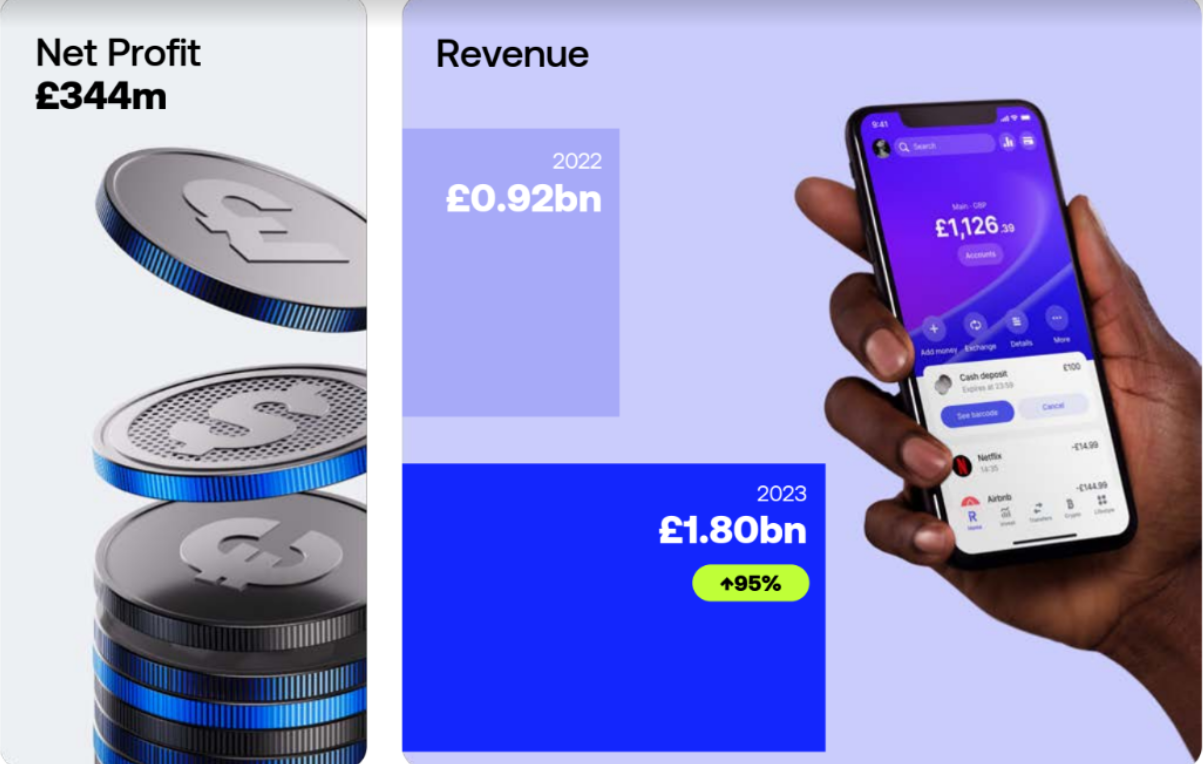

Nik Storonsky, CEO of Revolut said: “This year, we took our biggest steps yet on our mission to deliver the…

Revolut, the licensed European bank with more than 40 million customers around the world, has today announced that its <18…

EY today announces the launch of a new Sustainable Finance Innovation Hub in Dublin to help financial institutions around the…

Revolut, the global financial app with over 2.5 million customers in Ireland, warns that euphoria and urgency experienced by shoppers…

Exchange-traded derivatives, or ETDs, are financial agreements created by one or more parties, either people or companies. Through these agreements,…